What You Should Know

The Spending Boom: Healthcare now captures nearly half of all vertical AI spend, projected to hit $1.5 billion in 2025 (more than tripling from $450 million the year prior), according to the latest CB Insights State of Digital Health Q1’26 report. The Readiness Gap: Despite the massive investment, early AI pilots routinely fail. Less than 20% of enterprise healthcare data is currently ready for AI without substantial preparation.The Legacy Problem: Most healthcare data systems (like EHRs and CRMs) were built for billing, compliance, or sales tracking—not predictive modeling. This results in inconsistent data, such as mixed temperature units or non-standardized free-text diagnosis codes.The Rise of the “Mega-Round”

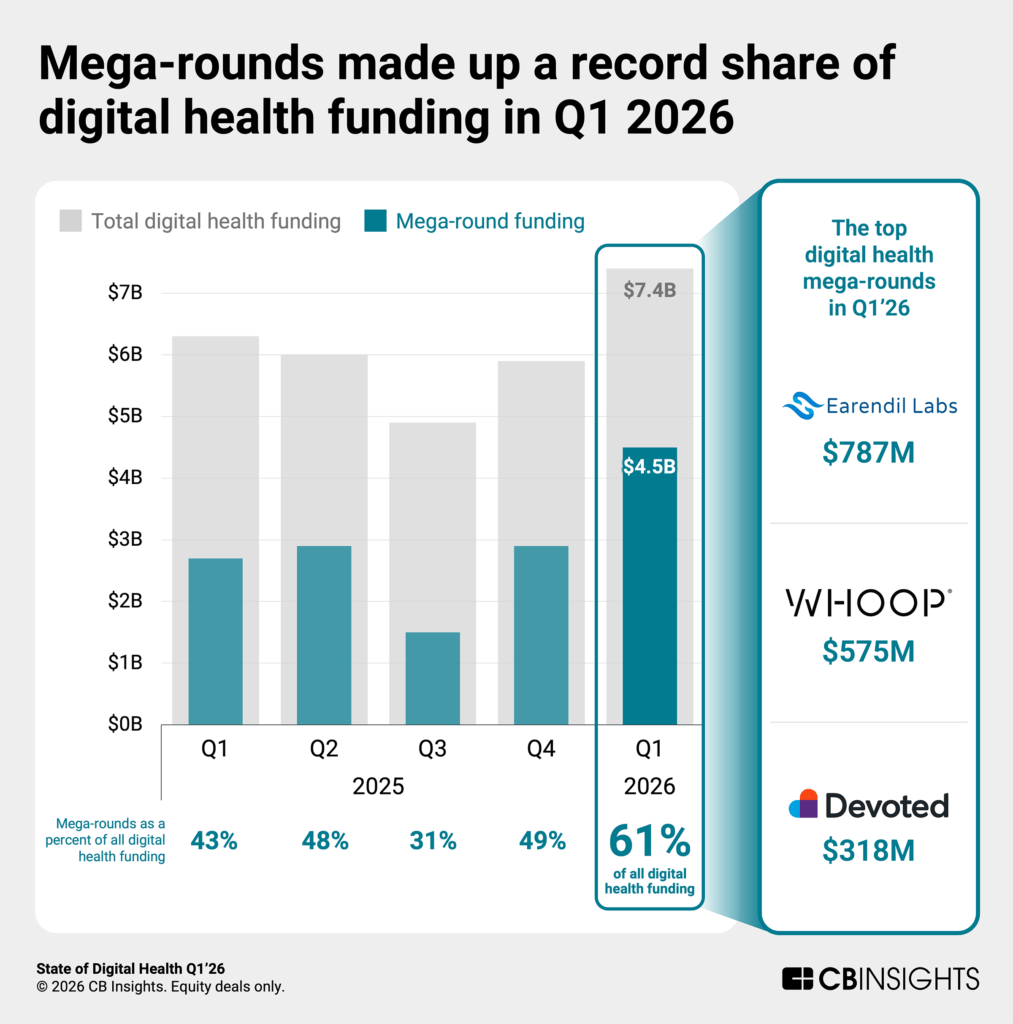

Funding in Q1’26 rose to $7.4B, a sharp increase from the $5.9B seen in the previous quarter. This growth was largely concentrated in 19 mega-rounds ($100M+), which accounted for 60% of all capital raised.

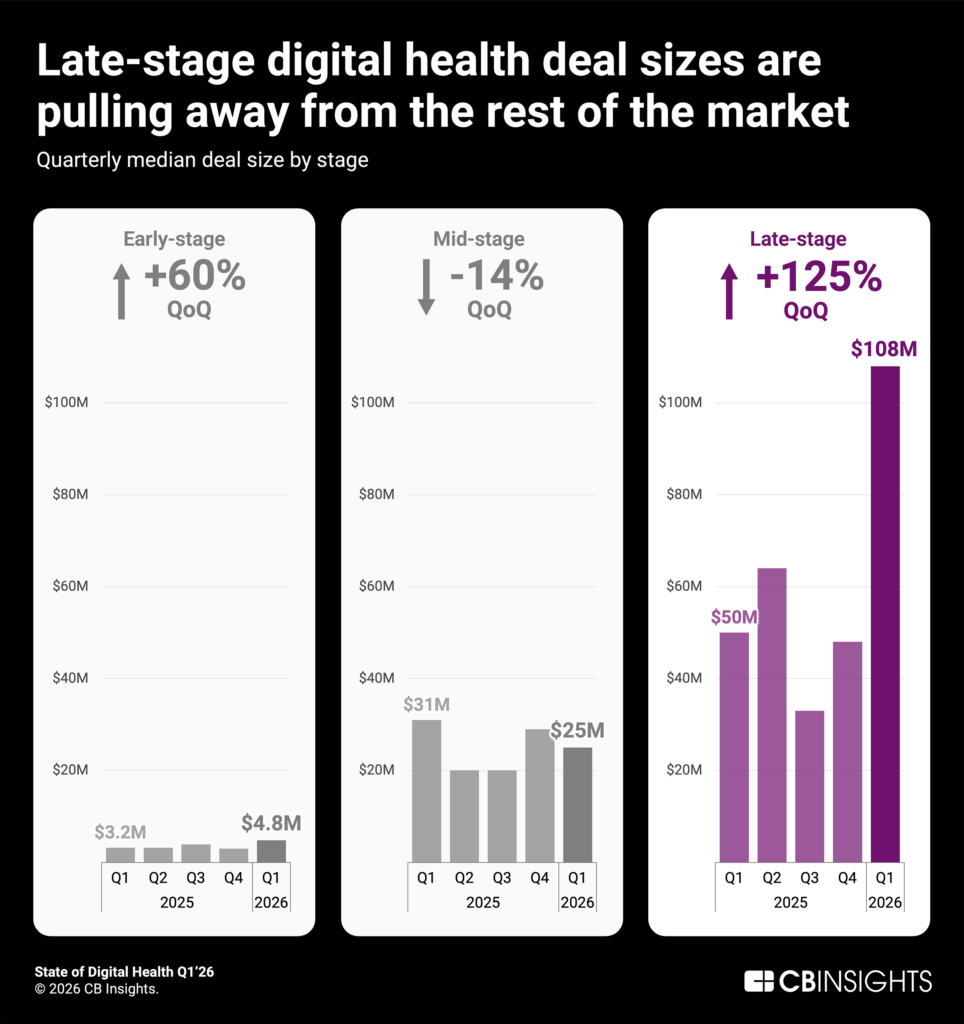

Late-Stage Dominance: The median late-stage deal size skyrocketed to $108M, more than double the $48M median from Q4’25.Unicorn Rebound: Eight new unicorns were minted this quarter—the highest single-quarter count in nearly four years.Market Leaders: Category leaders like Devoted Health and Alan are now operating with $100M+ war chests, allowing them to remain private while expanding their distribution and acquisition capabilities.M&A Strategy: Adoption Over Approval

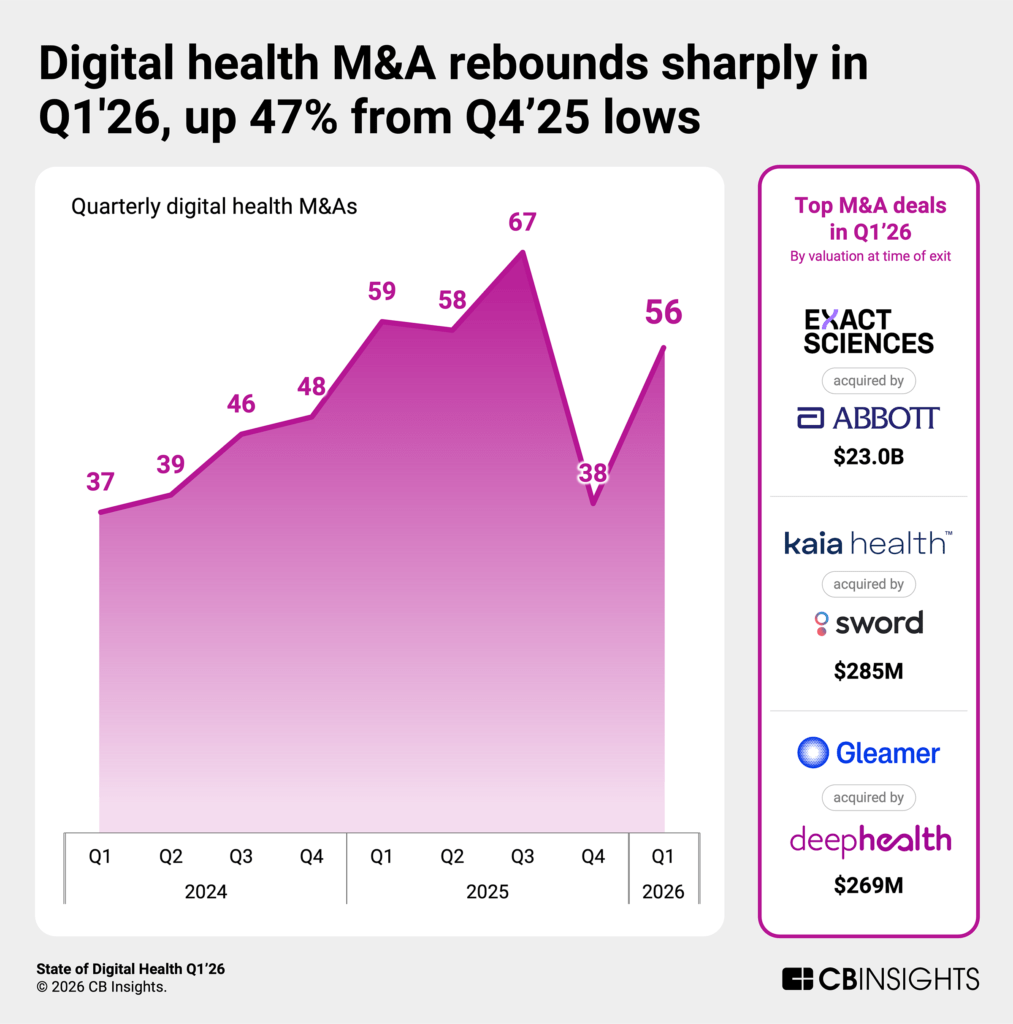

M&A activity jumped 47% this quarter, with 56 deals closed. The market is now strictly prioritizing commercial adoption over simple regulatory clearance.

Abbott’s $23B Bet: In the quarter’s largest deal, Abbott acquired Exact Sciences to take its proven Cologuard screening model global.The Adoption Premium: DeepHealth’s $269M acquisition of Gleamer was driven by a footprint of 700+ hospital contracts. Conversely, Oxipit—despite having a world-first autonomous AI certification—saw limited value due to negligible 2024 revenue ($27.6K).Prior Authorization: The 2027 Forcing Function

With the CMS-0057-F deadline mandating electronic prior authorization by January 2027, investment is flooding into the space.

Pure-Play vs. Platform: Latent secured an $80M Series A as a specialized provider, while Adonis raised a $40M Series C to expand its broader revenue cycle platform.Strategic Partnerships: Abridge and Availity collaborated to embed these capabilities directly into clinical workflows, while Samsung and b.well are integrating portable health records into Galaxy devices to meet CMS standards.AI Drug Discovery: Speed Meets Novelty

Pharma is committing billions to AI to compress research timelines.

Timeline Compression: Earendil Labs raised $787M—the largest deal of the quarter—to support a deep learning platform that has already generated 40+ therapeutic programs. Takeda also committed up to $1.7B to Iambic Therapeutics, which moved a candidate to IND in just 24 months (vs. the 6-year industry average).Novel Modalities: Early-stage capital is targeting platforms for new drug classes, such as Proxima ($80M for molecular glues) and Vibrant Therapeutics ($61M for macromolecular therapeutics).The Battle for Healthcare AI Talent

Headcount is growing rapidly as the market shifts from development to enterprise deployment.

Headcount Surges: Tennr and Hippocratic AI are leading hiring in the model developer market, with Hippocratic expanding into pharma R&D following its acquisition of Grove.Big Tech Competition: Anthropic grew its headcount by over 200% in the last year, launching a dedicated healthcare offering in Q1’26 to rival OpenAI.Infrastructure Layer: Nvidia is positioning itself as the underlying compute layer for the industry, recording 6 new digital health business relationships this quarter.For more information about the CBInsights Digital Health report, visit https://www.cbinsights.com/research/report/digital-health-trends-q1-2026/

Bengali (Bangladesh) ·

Bengali (Bangladesh) ·  English (United States) ·

English (United States) ·