3 hours ago

7

3 hours ago

7

Key Takeaways

Raoul Pal calls this a mid-cycle, not the end of the crypto cycle. He blames crypto’s underperformance on negative excess liquidity flowing to AI. He says excess liquidity has now turned positive, reopening the door for crypto. He’s personally accumulating layer ones at what he reads as oversold levels. These are his views and positions, not neutral analysis.Pal, the Real Vision CEO who earlier ran European hedge fund sales in equities and equity derivatives at Goldman Sachs from 1997 to 2001, laid out his case, arguing that crypto’s painful stretch is a liquidity problem rather than a broken thesis, and that he’s been buying.

Why Crypto Underperformed: A Liquidity Story

Pal’s core diagnosis is that crypto isn’t broken, it was starved. Excess liquidity, the amount of monetary growth above GDP growth, was negative for an extended period, and when excess liquidity is negative, capital flows to wherever it compounds fastest. That place was AI. As Pal put it, “if there’s no excess liquidity, it’ll find its home in the most compounding place. And the place that compounds intelligence the most is AI. So it compounded there.”

This ‘liquidity suction’ is a sentiment shared by industry leaders like Arthur Hayes and Michael Saylor, who both argue that AI’s current dominance has acted as a temporary drain on crypto capital. Their shared thesis suggests that once AI sector returns peak or cool, this capital is primed to rotate back into hard assets like Bitcoin as a strategic hedge against ongoing fiat debasement.

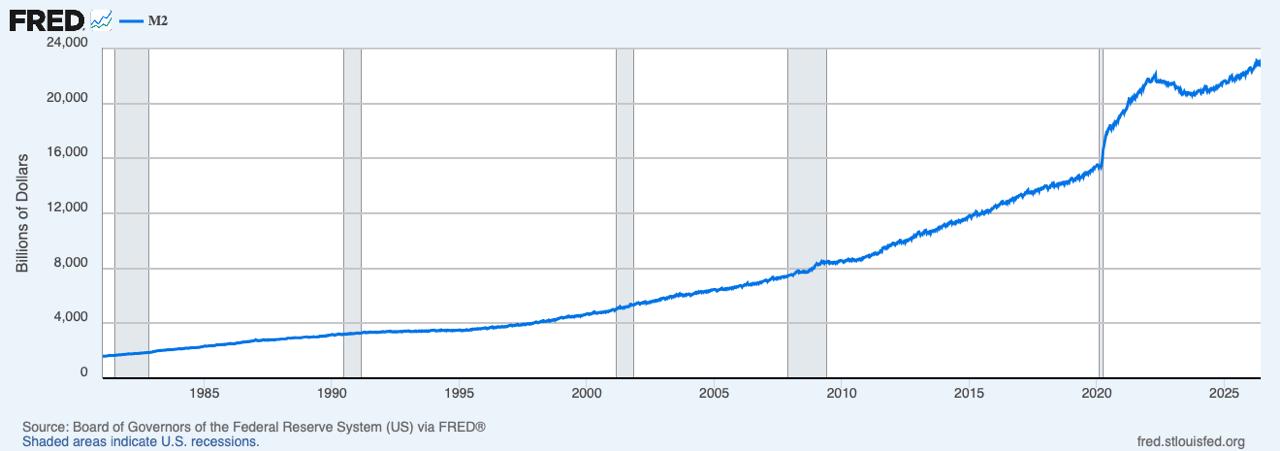

The shift he’s pointing to is that excess liquidity has now turned positive on both M2 and broader measures. In his framework, that changes the equation: more liquidity means more capital available for investments beyond AI, and that’s the opening through which crypto re-enters. As he summed it up, “we’ve got excess liquidity. It means there’s more liquidity for investments. And this helps us.”

U.S. M2 Money Stock (via FRED)

U.S. M2 Money Stock (via FRED)

Where He Thinks We Are in the Cycle

Pal calls the current moment mid-cycle, not a cycle end, and he leans on his technical framework to argue it. His log regression channel on Bitcoin is flashing oversold at roughly 1.5 standard deviations below fair value, the same signal, he says, that appeared at every prior major accumulation point. He points to Ethereum’s monthly DeMark indicators showing a full reversal pattern, and to SUI sitting 1.8 standard deviations oversold on its own channel. His conclusion: “the risk-reward on an adjusted basis going forward is extremely high.”

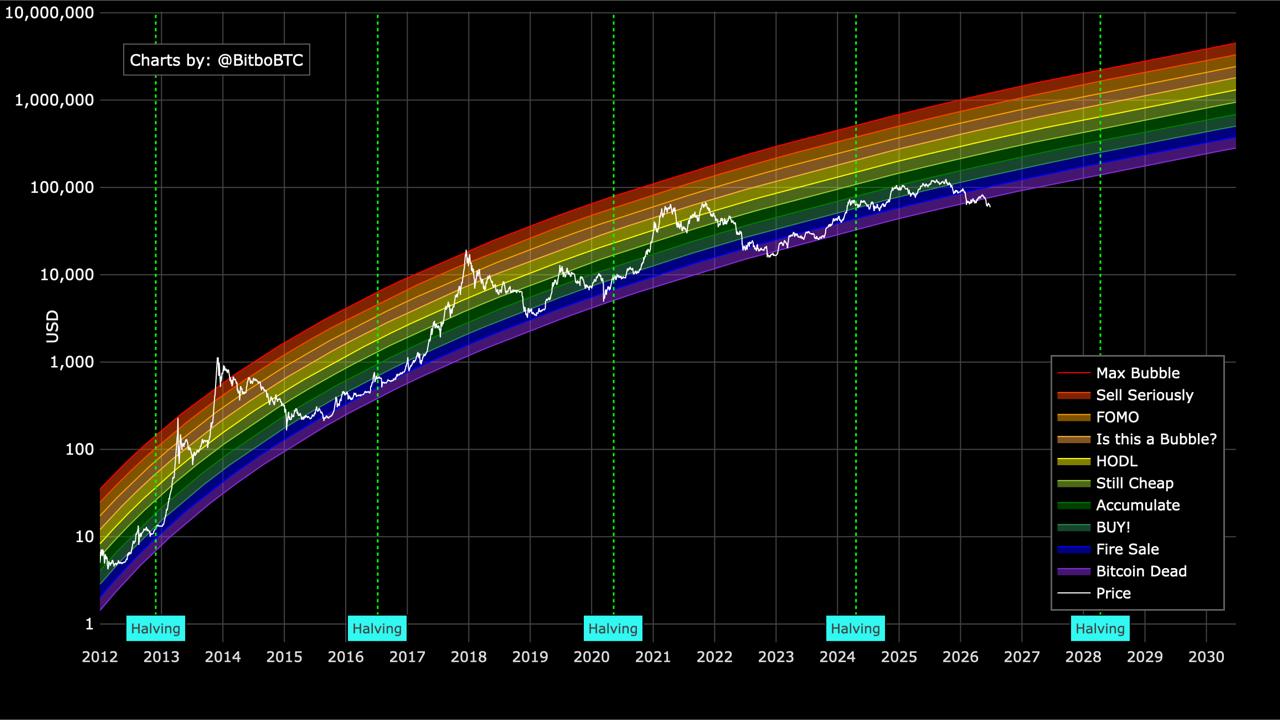

That positioning lines up with the Bitcoin Logarithmic Regression Bands, often shown as the “Rainbow Chart,” which map Bitcoin’s entire price history since 2012 against a long-term power-law trend and divide it into color-coded sentiment bands on a log scale. According to Bitbo’s charts, with Bitcoin around $59,500 on June 26, price sits below the model’s “Bitcoin Dead” band and into its lowest zone, deeper into oversold territory than any point in history.

Chart: Bitcoin Logarithmic Regression Bands (2012–2026)

Chart: Bitcoin Logarithmic Regression Bands (2012–2026)

Because the bands migrate upward over time, that placement is notable: every prior cycle bottom, in 2015, 2018-2019, and 2022, touched or briefly pierced these lower bands before recovering, with price returning to the higher “Accumulate” or “Still Cheap” bands within 12 to 18 months in each case.

The honest limit of the model is that it has no predictive mechanism built in. It’s a mathematical extrapolation of a 14-year trend, so it contextualizes where price sits against its long-term trajectory rather than forecasting where it goes next. It tells you this is historically low ground; it doesn’t tell you the bottom is in.

The contrast Pal draws is with semiconductors, which he reads as 3.8 standard deviations overbought versus their long-term trend. That gap between oversold layer ones and overbought semis is the relative-value setup he’s positioning around.

His Conviction on Layer Ones

Pal says his belief in the major smart-contract platforms hasn’t moved: “I strongly believe in Ethereum, Solana, Sui.” His reasoning ties crypto directly to the AI trend rather than treating them as rivals. Layer ones, in his framing, are the coordination, agentic, and value layers of the internet, and AI agents will need crypto rails to transact. He argues AI and blockchain are “married at the hip,” obvious to anyone actually using AI agents, because the programmable smart-contract layer is central to what’s coming.

His valuation point is blunt: it’s hard to argue NVIDIA doubles from here, but for Ethereum and Solana, he can see it. That asymmetry, limited upside in the crowded AI names versus more room in the beaten-down layer ones, is the case he’s making.

The Master Variable: Global Liquidity

Underneath all of it sits global liquidity, which Pal notes has an 85-to-87% historical correlation with Bitcoin and has been rising since 2022, when he went long. The current drag, in his read, is the strong US dollar, since dollar strength suppresses global liquidity in dollar terms. His expectation is that rates fall faster than expected, the dollar weakens, and liquidity accelerates. “The dollar’s too strong. That’s what’s causing this. I think that all changes,” he said. The setup he’s waiting for is excess liquidity firmly positive alongside a weakening dollar, the point at which the liquidity tailwind for crypto resumes.

The Rotation He’s Making

Pal frames the next move as a rotation of leadership, “the darlings that you hold won’t be the darlings that persist.” He says he’s trimming high-beta growth names like Rocket Lab and select semiconductors, on the reasoning that those assets have reached stretched valuations that effectively price in perfection and now offer an unfavorable risk-reward profile compared to the “unloved” layer ones sitting at cycle-trough support. The logic is symmetrical: semis at cycle-peak overbought levels, layer ones at cycle-trough oversold ones, and the rotation from one to the other is the trade he says he’s writing about for institutional clients.

On the discipline it takes to hold through the pain, he offered a familiar line: “the best performing brokerage accounts are the ones of dead people. It’s because they don’t sell.” His argument is that with a genuine thesis and framework, the right response to oversold conditions is accumulation, not panic. He says he’s added several positions around the current oversold level and is comfortable there, noting he’s been doing this since 2013.

The Honest Context

Pal’s framework is coherent, liquidity starved crypto, liquidity is turning, and the cycle has further to run, but a few things keep it in perspective. This is one investor’s read, built on his own indicators and macro calls, and those calls (rates falling faster than expected, the dollar weakening, liquidity accelerating) are forecasts, not facts. He is also personally positioned in exactly what he’s describing, accumulating the layer ones he’s bullish on, so his enthusiasm comes with that stake attached. The mid-cycle thesis is a genuine, well-argued view of where the market sits. Whether the liquidity tailwind he’s counting on actually arrives is the variable everything else depends on.

The post Ex-Goldman Sachs Exec on Where We Are in the Crypto Cycle appeared first on Coindoo.

Bengali (Bangladesh) ·

Bengali (Bangladesh) ·  English (United States) ·

English (United States) ·